Blog

Frozen protein has doubled since 2019. Has your surplus strategy kept up?

Frozen meat & poultry are hitting record highs in retail. See how meat suppliers are responding and recovering margin from fresh and frozen surplus.

WRITTEN BY

Amelia Smith

Published on

3/13/2026

Free KPI Toolkit

Start tracking your KPIs the same way leading CPG brands do.

Free KPI Toolkit

Start tracking your KPIs the same way leading CPG brands do.

Fresh surplus demands attention by default. With shorter shelf life and tighter windows than frozen, there’s no room for error in the distribution process. Frozen gets dealt with later because it can be. But "later" is becoming a more expensive strategy than most meat suppliers realize.

U.S. frozen food sales hit $87 billion in the 52 weeks ending September 2025, up more than 45% from 2019. More specifically, frozen meat and poultry have doubled to $8 billion in that same window — the single fastest-growing segment in the frozen aisle. Forty percent of consumers now use frozen products every few days or daily, up from 35% in 2019. Seventy-seven percent are buying frozen with a specific meal already in mind, and another 30% say they plan to buy even more. This is the strongest purchase intent measured in years.

When demand grows this fast, so does the volume of product that misses its primary channel window. And if your recovery process was designed around the urgency of fresh — reactive, manual, ad-hoc — it likely hasn't adapted to handle the frozen side of the equation.

The suppliers closing that gap share a common playbook. Here's what it looks like, and what their recovery numbers tell us about where the category is headed.

Fresh and frozen are both growing, and that's the problem

Despite what headlines might claim, frozen meat isn't replacing fresh, nor is it even necessarily outpacing it. Although frozen protein has skyrocketed in sales, both categories, when compared head-to-head, are projected to grow at roughly 3.7% CAGR over the next five years.

What is changing is how consumers use them together. According to AFFI reports, 76% now combine fresh and frozen in the same meal. When past shoppers might have been more segmented between the two, a shopper buying a pack of fresh chicken thighs for tonight is now the same shopper supplementing that with frozen veggies and convenient sides for their family. At the consumer level, fresh and frozen have become fully complementary categories.

That creates a compounding inventory challenge for suppliers managing both lines. Fresh meat surplus operates on tight shelf-life windows where every day of delay erodes value, and thus gets triaged first.

Frozen surplus is more forgiving on time but harder to move through ad-hoc channels that lack the right freezer capacity. The result, in many organizations, is that fresh gets the fire drill, frozen gets the back burner, and the same overtaxed team manages both with spreadsheets and phone calls.

The temptation is to think of this as a simple reallocation problem. If one category softens, shift production toward the other. But when both are growing at the same rate and consumers are buying both simultaneously, surplus compounds. And the frozen side — the side that's quietly deprioritized — is where we’ve identified an opportunity to get ahead.

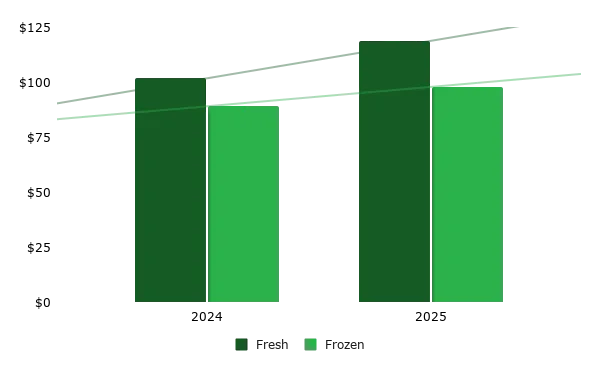

Protein Transacted Through Spoiler Alert YoY ($M)

What secondary market data is telling us

Spoiler Alert's platform processes over $200 million in fresh and frozen meat transactions annually across its buyer network, and the pattern emerging in the data is worth paying attention to.

Fresh meat surplus is flowing into secondary channels at more than 70% the growth rate of frozen. YoY, secondary markets purchased 16.7% more in fresh meats, compared to 9.8% growth in frozen over the same period.

That tracks with the urgency dynamic: fresh gets moved because it has to, and suppliers have built the muscle for it. Frozen, despite growing demand, is still catching up on the recovery side.

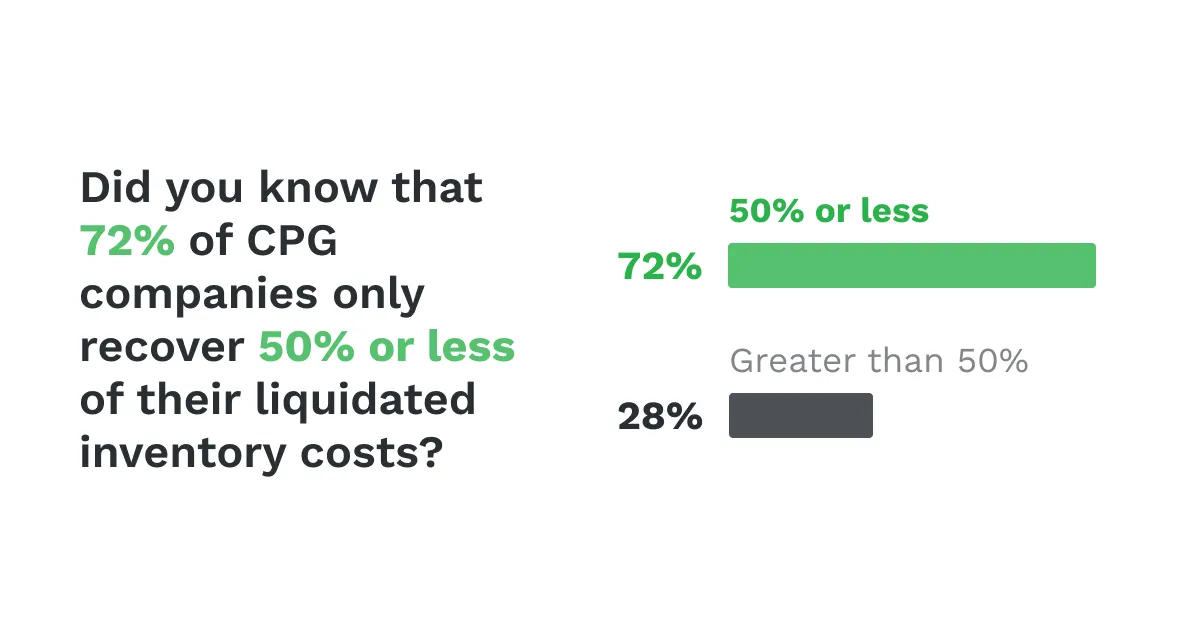

That gap represents real dollars left on the table. Brands shipping slow-moving, obsolete, and short-dated inventory through Spoiler Alert see a sell-through rate of 86.86%, nearly double the 48% that CPGs report on average when surveyed about their excess inventory programs.

Where the buyer side is headed, and how suppliers are responding

The buyer side of the secondary market is scaling to match. The surplus food redistribution market is growing at approximately 7.8% CAGR — roughly double the growth rate of either meat category — and valued at an estimated $56.8 billion.

The secondary market used to lack the capacity to absorb frozen volume at scale. That constraint is disappearing fast with discount retailers continuing to add freezer and cooler capacity with each new opening. This means it’s time for suppliers to respond. The suppliers plugged into these channels are recovering real margin on inventory that would have otherwise been written off.

The suppliers getting this right aren't treating surplus as an afterthought

The brands recovering the most value from excess inventory have one thing in common: they've stopped letting shelf life dictate which surplus gets attention. Fresh and frozen both get a systematic recovery process, run through the same platform, and with the same buyer network. The question is whether your operation has made that shift, or whether frozen is still waiting its turn.

To learn more about how our software and solutions can help your organization to turn excess inventory into opportunity, book an intro call with our team today!

WRITTEN BY

Amelia Smith

Published on

3/13/2026

Don't miss our latest Stories — Stay Inspired!

.png)