She earns $140,000 a year. She drives a Lexus SUV. And on Saturday morning, she's pushing a cart through Grocery Outlet. She's not there because she has to be; she's there because she discovered a premium sparkling water brand at 50% off last month, tried it, loved it, and bought a case at full price the following week from her local Whole Foods.

She is not an anomaly. According to Martie, 83% of consumers who discover a brand through a discount channel will go on to repurchase that product at full price. And yet CPGs still meet the discount channel with hesitance that liquidating their premium SKUs to closeout retailers will damage brand perception.

The shopper profiled above represents a demographic shift that most CPG commercial teams still haven't internalized. Nearly 28% of high-income consumers, households earning $169,000 or more, shopped at discount chains in 2025, up 40% since just 2021.

These are highly sought-after consumer segments actively choosing the discount channel because persistent inflation, pricing anxiety, and the destigmatization of discount shopping have made treasure hunting a mainstream behavior, and this represents three shifts in the modern CPG paradigm:

- The discount channel is one of the most untapped brand growth environments in US retail.

- The consumers shopping at discount grocers are exactly the segments brands are seeking.

- Closeout retailers know this, and do more to protect brand equity on the shelves than ever.

The 2 fears that build the wall

Ask a CPG brand strategist why they hesitate to work with closeout wholesalers, and you'll hear two objections repeated so consistently across the industry, they're practically treated as law.

The first is diversion: the fear that product sold into the secondary channel will boomerang back into a brand's primary retail partners, undercutting full-price sales. That’s because some wholesalers will distribute closeout products to their own network of retailers. Mark Fleming, CEO of Natural Choice Foods (NCF), one of the largest closeout wholesalers in the CPG industry, has something else to say.

Before speaking with Spoiler Alert in a webinar, Fleming spent thirty years on the manufacturing side before crossing over to run NCF, which gives him a rare vantage point on both sides of the transaction. In the webinar, he shared how NCF and fellow wholesalers in the industry account for these diversion fears.

"NCF provides every manufacturing partner with its complete customer list before a single pallet ships. If customer overlap exists, even a theoretical one like a retail buyer who vacations in a market where NCF sells, we turn that geography off.” - Mark Fleming, CEO & President, Natural Choice Foods

The second objection is brand dilution: the worry that a consumer seeing your brand on a closeout shelf will damage their perception of said brand.

"In thirty years in food manufacturing, I've never seen any factual evidence that supports it,” Fleming said when asked about it. “I've heard the conceptual argument over time, but I've never seen a study or any research that says the closeout buyers diminish the brand," Fleming responded.

That absence of evidence matters – the entire industry has organized supply chain strategy around a fear that no one has been able to substantiate.

Meanwhile, the evidence for the opposite keeps accumulating.

Why the consumer shift is here to stay

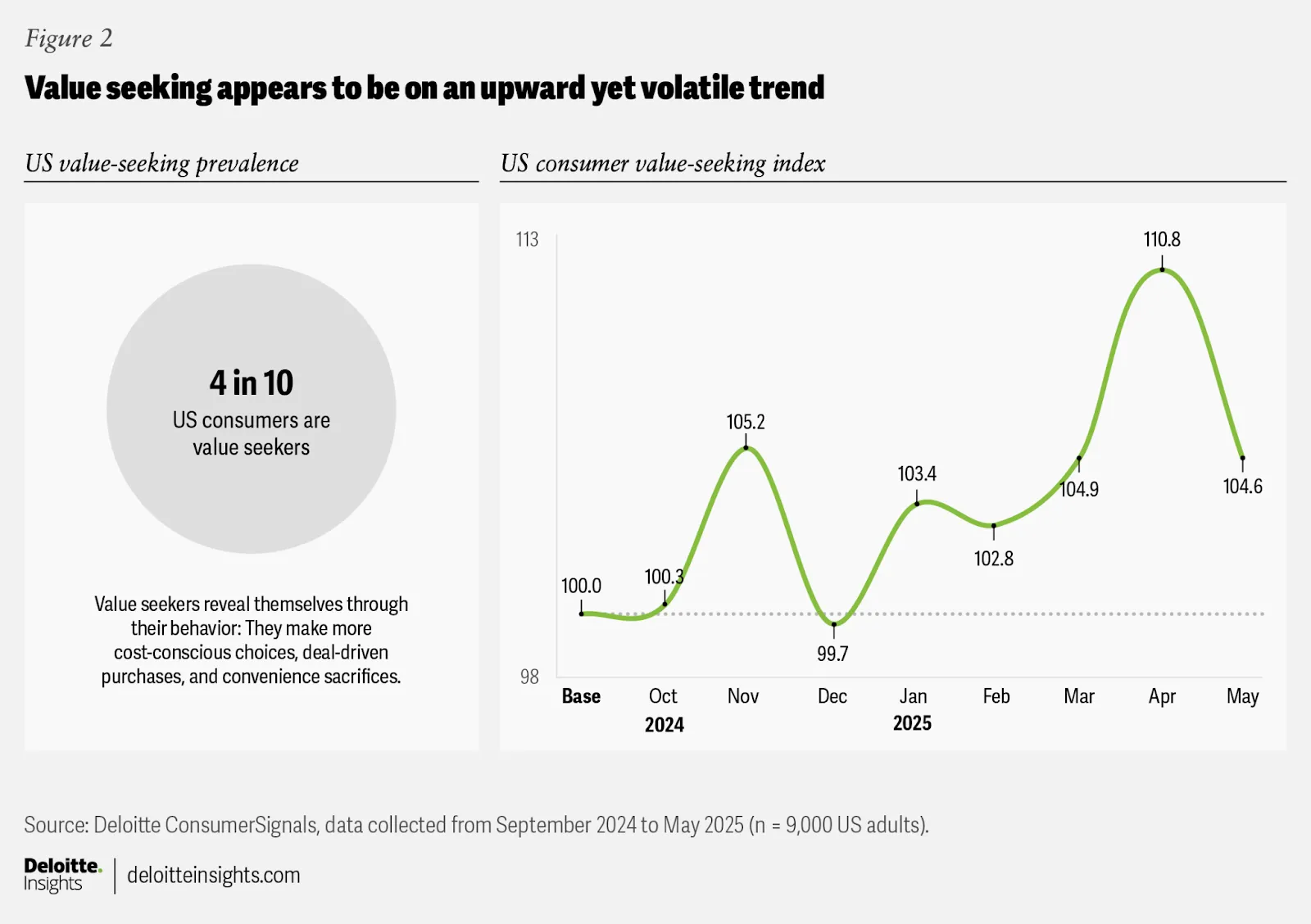

McKinsey's August 2025 ConsumerWise survey found that 75% of U.S. consumers planned to trade down in some form. Deloitte's ConsumerSignals research, tracking 900,000 consumer data points, found that four in ten Americans now qualify as "value seekers" – and that the behavioral effect is strongest among households earning $200,000 or more, who planned to cut discretionary spending by 50–60% relative to their peers.

The foot traffic confirms it, too. Placer.ai data shows off-price retailers now receive more total visits than traditional department stores, which is a reversal from 2019. During the 2025 holiday season, off-price visits grew 6.6% year over year, thrift stores jumped 11.7%, and wholesale clubs rose 7.5%, all outpacing the overall retail average of 2.8%.

The customer your brand is trying to "protect" from seeing your product at a discount retailer is already shopping there, finding new premium brands to fall in love with.

What discount retailers actually look like up close

In response to these shifts, closeout buyers and secondary retailers have adapted how they protect the brands on the shelves.

Grocery Outlet calls itself a "preferred CPG partner for a non-disruptive, brand-protected sales channel." That language is deliberate. The company works with brands from General Mills and Nestlé to emerging players like Poppi and Olipop, pricing products 40% below conventional grocers and 20% below Walmart. Its independent operator model gives each of its 570 stores the latitude to customize assortments locally, which creates a built-in scarcity mechanism.

TJX CEO Ernie Herrman said directly on the Q4 FY2026 earnings call in February, "We are going after brands in a more aggressive manner than we ever have before. We mean more to the branded vendor community than ever." Retail Brew reported in March 2026 that TJX is evolving from a pure liquidation channel to a regular buying partner, combining opportunistic purchases with scheduled buys and formal management-level meetings with key brand partners.

Ross Stores warehouses seasonal branded goods at favorable prices for later selling seasons through its "packaway" strategy. $22.8 billion in fiscal 2025 revenue. Morningstar assigns Ross a wide economic moat rating. Like TJX, its physical-store focus limits the visibility of discounted prices.

At Ollie's Bargain Outlet, roughly 70% of purchases are brand-name closeouts. CEO Eric van der Valk has been explicit about leaning into market volatility: "Our model thrives on disruption. Tariffs have created uncertainty in the market, which is disruptive. This has resulted in additional buying opportunities." The company opened 86 new stores in fiscal 2025, reaching 645 locations.

Natural Choice Foods operates differently from these publicly traded giants, but its position in the channel is revealing. NCF serves independent grocers – many in food deserts where shoppers would otherwise drive 40 to 60 miles to reach a big-box store. Their five retail stores in Grand Rapids recently won recognition from Shelby Report and Progressive Grocer. "Our stores literally sit side by side with some major, major retailers," Fleming told us. "It's not disruptive to it. It fits within it very neatly."

These buyers are not only a safe haven for brands to recover margin on their surplus inventory; they’re a destination for brand growth amidst volatile market conditions.

How brand protection has evolved in the discount channel

Each major player in this channel and within the Spoiler Alert network has built structural brand protection into how it operates.

Minimum Advertised Price (MAP) policies remain the primary guardrail, structured as unilateral policies under the Colgate doctrine to avoid antitrust liability. MAP policies also commonly include explicit exceptions for closeout and discontinued products, permitting deeper discounting once a product passes specific lifecycle thresholds. The pathway for goods to flow into secondary channels is already structured into the brand's own pricing architecture. And 53% of unauthorized retailers violate MAP policies according to Vorys, a law firm specializing in brand enforcement.

The real risk sits with gray-market resellers the brand never authorized, not with closeout buyers operating under established agreements.

Operational

Retailers like NCF are prescriptive and intentional in how they approach brand protection. NCF, for example, picks up product directly from the manufacturer, warehouses it in their own facilities, and delivers roughly 80% of what they sell via their own fleet. If a manufacturing partner doesn't want product sold in a particular region, NCF modifies its customer base accordingly.

"We provide them our customer list. They know exactly where we sell," Fleming told us. This level of control is the opposite of the "throwing it into the void" narrative that the diversion fear is predicated on.

Fleming also described NCF's repackaging services. Food-service packages, the 40-pound boxes, can be converted into three- or five-pound retail units. Private-label products can be stripped, debatched, and repackaged under brand guidelines. As such, the original retail partner's shelf set is never touched.

Structural

TJX and Ross, the two largest off-price retailers in the country, do almost no e-commerce by design. TJX blocks brand-name search filtering on its website entirely, preventing consumers from searching by brand. A deliberate move to protect brand partners from visible markdowns. Compare that with a department store running an online clearance sale that any consumer (or competitor) can find in three seconds. The physical-store architecture of the off-price model is itself a brand-protection mechanism.

The treasure-hunt dynamic reinforces this. Inventory rotates constantly, with brands appearing "sporadically and covertly", which prevents any single brand from becoming mass-associated with discount pricing. TJX's strategic repositioning from "discount retailer" to "treasure hunt destination" helped the company nearly double annual sales between 2014 and 2024. The scarcity that defines these stores is what keeps brands safe inside them.

The cost of waiting

Every day a manufacturer holds excess inventory hoping for a primary-channel miracle, two things happen: the warehouse carrying costs go up, and the recoverable value of the SKUs go down.

Fleming has watched this play out from both sides: "You're paying to warehouse it. You're paying for a management team to think about it. And every day that goes by, the value you can sell it for drops precipitously."

He described the concept of "shippable life," the threshold in which major retailers will accept product based on remaining shelf life. Once a frozen product crosses about six months, most big-box retailers won't touch it. Not because the product is bad, but because their own supply chain scale requires a cushion. The product is still perfectly good, but it's on the wrong side of a line that most manufacturers' planning teams treat as a cliff.

After all, the old industry adage applies: your first loss is your best loss. And from Mark’s words, "If your product isn't going to sell through primary channels, stop investing in it.

“If your product isn’t going to sell through primary channels, stop investing in it.” – Mark Fleming, CEO & President, Natural Choice Foods

The surplus pool feeding this channel keeps growing. Industry estimates suggest 20–30% of all CPG stock goes unsold. Tariff-driven front-loading pushed record volumes through U.S. ports in 2025, creating massive inventory overhangs. Global energy crises are creating a supply chain nightmare that will inevitably hurt manufacturers and consumers the most. Even legislation, like California's SB 1383, has started fining brands for landfilling overstock, making secondary-channel distribution even more fiscally advantageous than destruction.

The discount sector now accounts for roughly 30% of all planned U.S. store openings in 2025. The channel is expanding, and the consumer is already there. The question is whether your brand will be too.

Where the three circles overlap

Fleming has a slide he uses when talking to retail partners. It consists of three overlapping circles:

- One for manufacturers carrying a P&L drain from excess they can't move.

- One for independent retailers who don't have efficient access to the brands their shoppers want.

- One for consumers, from food-insecure families to value-seeking suburbanites, who are looking for quality brands at prices that work.

"Where those three overlap," he told us, "is a marketplace that [Spoiler Alert] and I are managing and activating and creating. We're helping the manufacturer, we're helping the retailer, and we're helping the consumer."

Remember the woman from earlier – The one earning $140,000 and pushing a cart through Grocery Outlet on a Saturday morning? She found a brand at a discount, trying it because the price made the trial painless. She later went back to her regular store and bought it at full price. That's not brand erosion; that's one of the most efficient customer acquisition tactics in CPG, and it's been hiding in a channel most brands have spent decades avoiding.

Natural Choice Foods is one of hundreds of vetted secondary buyers that brands can reach directly through Spoiler Alert. Spoiler Alert is the excess inventory management platform that connects CPG manufacturers with an active network of discount, off-price, and closeout wholesalers.

It replaces the email chains and spreadsheets the process used to run on with automated workflows, dynamic pricing based on remaining shelf life, and built-in channel governance, turning surplus inventory into recovered margin without compromising primary retail relationships or brand equity.

Natural Choice Foods and Spoiler Alert hosted a live conversation on how brands can participate in the secondary channel with confidence. Watch the full webinar to learn more.